Wholesale, Professional Investors and Advisers only

The information, products and services described in this website are intended solely for persons in Australia who are wholesale clients within the meaning of section 761G of the Corporations Act 2001 (Cth), and is not directed at persons located in the United States and its territories and is not intended to be available to U.S. persons as defined under Regulation S of the U.S. Securities Act of 1933, as amended.

By clicking Confirm below, you confirm that:

You are a wholesale client for the purposes of section 761G of the Corporations Act 2001 (Cth); and

You are not a “U.S. person” as within the meaning of Regulation S of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and are not investing for the direct or indirect benefit of a U.S. Person as within the meaning of Regulation S under the Securities Act; and

You accept all of the Terms and Conditions of this website.

The missing piece in private credit portfolios? A closer look at Asset Backed Finance

August 1, 2025

Rethinking diversification in private credit – Luke Mandekic of Channel Capital shares why traditional approaches may no longer be enough and how new solutions like Asset Backed Finance can enhance portfolio construction.

As fixed income markets continue to evolve, advisers are facing a common and growing challenge: how to deliver consistent income, manage downside risk, and diversify exposures, all while navigating an uncertain interest rate environment. For many, traditional corporate credit has been the go-to solution. But increasingly, advisers are looking beyond this to explore new ways to strengthen portfolio construction.

One area that is heavily utilised among institutional investors and is now becoming more accessible to sophisticated wealth clients is Asset Backed Finance. For advisers, it presents a compelling opportunity to broaden credit exposure, reduce correlation to traditional credit markets, introduce additional risk premiums, and access stable, real-economy-linked income streams.

So what exactly is Asset Backed Finance, and how can advisers position it with clients?

What is Asset Backed Finance?

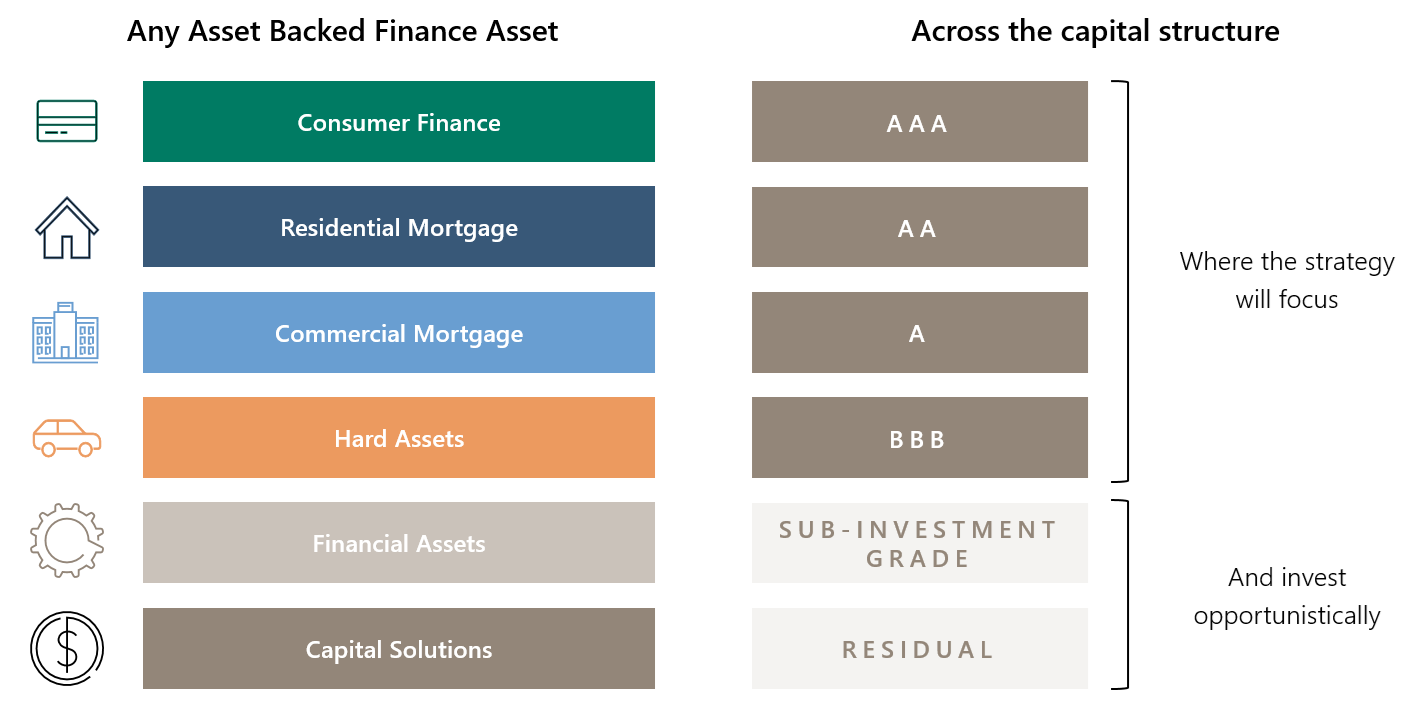

At its core, Asset Backed Finance is a form of private lending secured by pools of tangible or financial assets. These might include residential mortgages, auto loans, aircraft leases, equipment financing, infrastructure receivables, or even recurring contractual cash flows.

Unlike corporate lending, which relies on a company’s ability to repay based on its earnings and balance sheet, Asset Backed Finance is concerned only with the performance of the underlying assets. That means the loan isn’t backed by the solvency of a business, but by a predictable stream of repayments coming from real-world assets.

Put simply, you’re lending against the cash flows of the assets themselves, not the creditworthiness of a company. That shift changes everything, from how risk is assessed, to how returns are generated, and how portfolios behave through different market cycles.

Investors are also protected by structural features including credit enhancement, diversity of collateral, and subordination, designed to absorb losses before investor capital is impacted. This adds a layer of capital protection not always present in corporate loans, where recoveries depend on restructuring outcomes.

Asset Backed Finance typically involves senior secured lending, where each loan is backed by tangible or contractual assets. Collateral types can include:

Why is Asset Backed Finance worth considering now?

We’re at an inflection point in the credit cycle. As central banks slowly pivot from tightening to easing, advisers are increasingly grappling with reinvestment risk. Term deposits are rolling over at lower rates. Floating rate credit is offering less yield than it did 12 months ago. Meanwhile, credit spreads are tight, and the “easy money” in credit may be behind us.

Against this backdrop, clients are looking for solutions that still deliver income but also offer capital resilience and flexibility. This is where Asset Backed Finance can play a meaningful role. It often delivers attractive income, but it does so with a very different risk and return profile to corporate credit. It’s less dependent on corporate solvency, and more reliant on broad-based cash flows tied to the real economy.

Further, many Asset Backed Finance strategies are designed with the ability to include both fixed and floating rate exposures, providing more diversity and flexibility to manage the full interest rate cycle, while still preserving yield.

How does it fit into private credit portfolios?

In the Australian market, most private credit exposure is heavily skewed towards corporate lending, particularly to small and mid-market or property-linked borrowers. These exposures tend to cluster around a narrow set of economic risks including business defaults, balance sheet deterioration, and market-specific downturns.

Asset Backed Finance complements this by offering something fundamentally different.

First, it introduces diversified sources of income. Rather than relying on one borrower’s solvency, a diversified Asset Backed Finance portfolio may be made up of thousands of individual loans or receivables, each contributing a small piece to the overall return. That diversification helps to reduce the impact of any single default.

Second, Asset Backed Finance is typically senior secured. That means loans are backed by real collateral, be it property, vehicles, equipment, or contracts, and often benefit from structural protections such as credit enhancement, subordination (which provides a hierarchy of protection), or overcollateralisation (which provides an additional buffer). These mechanisms are designed to absorb losses before investor capital is impacted. Put simply, these structural protections provide a built-in layer of protection that helps improve the credit quality of an investment.

Third, it gives clients exposure to parts of the economy not easily accessed through public or corporate debt markets. Think of sectors like housing, transport, consumer finance, or trade infrastructure. These cash flows tend to be more stable and less cyclical than corporate earnings, particularly in times of market stress.

Relative to private corporate debt, Asset Backed Finance portfolios can offer superior credit quality (much of the market is investment grade) with similar returns and enhanced liquidity (deep public and secondary markets for Asset Backed Finance securities exist). The incremental yield that Asset Backed Finance can achieve is largely attributable to the complexity involved in the securitisation process and evaluating these structures. For investors that are able to access this complexity premium, it can bring attractive diversification and return enhancement to portfolios.

A word on risk and structure

Understandably, some clients may hear the term “asset backed” and think back to the GFC. But it’s important to stress that the Asset Backed Finance market of today is a world apart from the pre-2008 era.

Since the GFC, regulation and oversight have fundamentally reshaped this part of the market. Underwriting standards are more conservative. Transparency has improved. Complex, opaque structures have been replaced with simpler, investor-friendly designs. Importantly, most institutional Asset Backed Finance exposures today sit in senior (Investment Grade or equivalent), well-collateralised positions, rather than the high-risk equity tranches that caused problems in the past.

And the investor base has changed. Institutions such as pension funds and insurance companies now dominate Asset Backed Finance markets, making very long-term investments in the sector and bringing with them a greater focus on credit quality, risk management, and capital preservation.

So how should advisers approach the conversation?

For clients seeking yield, stability, and diversification, especially those already allocated to high yield corporate credit, Asset Backed Finance is worth introducing as a complementary strategy. It allows advisers to shift the conversation beyond company default risk and towards structural protections, income resilience, and exposure to real assets.

The key is to keep the explanation simple and relatable. For example:

“Rather than lending to companies, this approach lends to pools of assets like mortgages or leases, where returns are driven by stable contractual cash flows, and your investment is secured by real assets, not a company balance sheet.”

It’s also important to frame Asset Backed Finance as a long-term, income-oriented investment. While it is generally illiquid, the trade-off for this is greater control, security, and yield potential, especially when managed by experienced institutional platforms.

Challenging the old playbook

Asset Backed Finance is not a replacement for corporate credit, but an addition to help diversify client portfolios. It can bring a different set of risk drivers, more granular diversification, and meaningful protections in a market that continues to challenge traditional income strategies.

For advisers, it’s an opportunity to introduce clients to a more evolved way of thinking about private credit, one that aligns with today’s environment and helps prepare for whatever comes next.

As the credit landscape evolves, reassessing long-held assumptions about fixed income can help ensure portfolios remain well-positioned for the road ahead. Asset Backed Finance represents one way to add depth and diversification to this process.

Luke Mandekic is co-head of distribution at Channel Capital. For more information, contact us.

This communication is intended solely for professional and wholesale investors and has been issued by Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML'). CIML is the responsible entity and issuer of units in the Apollo Asset Backed Credit Trust (AUD) ARSN 684 032 291 (the ’Fund’). Channel Capital Pty Ltd ACN 162 591 568 AR No. 1274413 (‘Channel Capital’) is the holding company of CIML and distributor of the Fund. The Fund invests in the Apollo Asset Backed Credit Company LLC (the ‘Underlying Company’, or together with its affiliates, ‘Apollo’). Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Channel Capital or Apollo to buy, sell, or hold any security. Views and opinions are current as of the date of this document and may be subject to change, they should not be construed as investment advice.

Neither CIML nor Apollo, their officers, nor their employees make any representations or warranties, express or implied as to the accuracy, reliability, or completeness of the information contained in this email. Nothing contained in this email is or shall be relied upon as a promise or representation, whether as to the past or the future. Past performance is not a reliable indication of future performance. Where CIML or Apollo relies on third parties to provide information used in this email, CIML or Apollo, their respective directors and their respective employees, are not responsible for the accuracy of that information. The opinions expressed herein reflect the judgement of CIML and/or Apollo at the time of this publication and are subject to change. Subsequent changes in circumstances may also affect the accuracy of the information. CIML and Apollo do not provide any guarantee about the future performance of the investment products, managers, asset classes or capital markets discussed.

This information is given in summary form and does not purport to be complete. Information in this media statement should not be considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units in the Fund and does not take into account your particular investment objectives, financial situation or needs. All investments contain risk. An investor should, before making any investment decisions, consider the appropriateness of the information in this communication, and seek professional advice having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice. For further information and before investing, please read the Product Disclosure Statement and Target Market Determination available at www.channel-apollo.com.au.

To the maximum extent permitted by law, none of CIML, Apollo their directors, employees or agents accepts any liability for any loss arising, including negligence, from the use of this media statement or its contents. It does not constitute an offer to sell or a solicitation of an offer to purchase or advice in relation to any securities within or of units in any investment fund or other investment product described herein.

Subscribe

Please keep me updated with the latest information on the Fund and any investment insights.

This information has been prepared for use only by wholesale clients (as defined under the Corporations Act 2001 (Cth)).

Channel Investment Management Limited ACN 163 234 240 AFSL 439007 (‘CIML’) is the responsible entity for the Apollo Asset Backed Credit Trust (AUD) ARSN 684 032 291 (the ‘Fund’). Neither CIML, the Underlying Company (Apollo Asset Backed Credit Company LLC, (the 'Underlying Company', or together with its affiliates "Apollo")), Apollo, their affiliates, its officers, or employees make any representations or warranties, express or implied as to the accuracy, reliability or completeness of the information contained on this website and nothing contained on this website is or shall be relied upon as a promise or representation, whether as to the past or the future. Apollo and its affiliates have not been involved, except as otherwise stated, in the preparation of this website. In addition, Apollo and its affiliates are not involved in the investment recommendation or decision-making process for the Fund. Past performance is not indicative of future performance. This information is given in summary form and does not purport to be complete. Information on this website should not be considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units in the Fund and does not take into account an investor’s particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice. For further information and before investing, please read the Fund's Product Disclosure Statement and Target Market Determination available from www.channel-apollo.com.au.

Any interests expressed is taken as an indicative intention only and is not binding on the investor or CIML.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by CIML or Apollo or its affiliates to buy, sell, or hold any security. Views and opinions are current as of publishing and may be subject to change, they should not be construed as investment advice. This material on the Underlying Company is provided for educational purposes, in the context of the distribution of the Fund only and should not be construed as investment advice or an offer or solicitation to participate in the Underlying Company.

This website has been prepared, and all information regarding the Fund is provided, by CIML for use only by wholesale clients. To the extent any information provided by Apollo involves the provision of financial services in Australia under the Corporations Act 2001 (Cth), such information is provided by Apollo Management Singapore Pte. Ltd., and the following disclosure applies: Apollo Management Singapore Pte. Ltd. is exempt from the requirement to hold an AFSL under the Corporations Act 2001 (Cth) for financial services provided to wholesale clients. It does not hold such a licence and is regulated by the Monetary Authority of Singapore under Singaporean laws, which differ from Australian laws.

Certain information contained herein may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results or the actual performance of the Fund may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such information. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.